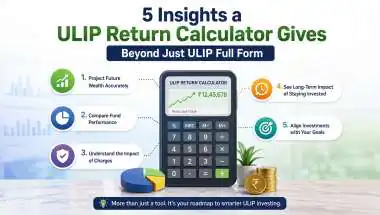

5 Insights a ULIP Return Calculator Gives Beyond Just ULIP Full Form

Discover five powerful insights a ULIP return calculator reveals about your investments, from projected maturity value to risk-adjusted growth, helping you make smarter financial decisions.

ST Webdesk Verified Media or Organization • 13 Apr, 2026Editorial Desk

June 2, 2026 • 6:32 PM

B

Business

NEWS CARD

“5 Insights a ULIP Return Calculator Gives Beyond Just ULIP Full Form”

Read more onwww.sangritoday.com/s/b651c4

2 Jun 2026

https://www.sangritoday.com/s/b651c4

Copied

5 Insights a ULIP Return Calculator Gives Beyond Just ULIP Full Form (AI Generated Image)

Most people who search for ULIP stop at the full form. ULIP is Unit Linked Insurance Plan.

They read the definition. Understand it is a mix of insurance and investment. And then close the tab.

It does a lot more than just show you maturity returns. Here are five things it reveals that most people completely miss.

Insight 1: How Much of Your Money Actually Gets Invested

This one surprises most people.

When you pay a ULIP premium, not all of it goes into investments. A portion is deducted as charges first. These include:

● Premium allocation charge: deducted before investing

● Policy administration charge: deducted monthly

● Fund management charge: deducted from the fund value

● Mortality charge: for the life cover portion

A ULIP return calculator shows you the exact amount that gets invested after all these deductions. For example, if you pay ₹1 lakh per year, maybe ₹94,000 actually enters the fund. The rest goes towards charges.

This is not a bad thing. But knowing it helps you plan better. You are not guessing. You are seeing the real numbers.

Insight 2: The Difference Between Funds Makes a Huge Difference

A ULIP lets you choose where your money gets invested. Equity funds. Debt funds. Balanced funds.

Most people pick one and forget about it.

But a ULIP return calculator lets you compare. Enter the same premium amount. Same tenure. Now switch between an equity fund at 10% expected return and a debt fund at 6%.

The difference in maturity value over 20 years can be several lakhs — sometimes even crores for larger investments.

This insight helps you match your fund choice with your actual risk appetite. Someone close to retirement should probably not be sitting in a high-equity fund. A young earner in their 20s can afford to take more risk.

The calculator shows you this visually. Numbers make it real.

Insight 3: What Happens If You Stop Paying Midway

Life is unpredictable. Jobs change. Expenses rise. What if you cannot keep paying premiums after year 5?

A good ULIP return calculator models this scenario.

It shows you:

● What your fund value looks like if you stop at year 5

● Whether the policy becomes paid-up or lapses

● How the remaining corpus grows even without new contributions

● What you will receive at maturity versus if you had continued

This is called a lapse scenario analysis. Very few people think about this before buying. But it is one of the most important things to check.

Because a ULIP is a long-term commitment, usually 10 to 20 years. Knowing what happens if you exit early helps you decide how much premium you can genuinely commit to.

Insight 4: The Tax Benefit Is Bigger Than You Think

Tax is boring to think about. Until you realise how much of your money it takes.

ULIPs have a quiet advantage here. You save tax going in, premiums up to ₹1.5 lakh qualify under Section 80C. And if conditions are met, the entire maturity amount comes out tax-free.

Other investment products do not always give you both.

Here is a real comparison. Two products. Both earn 10% annually. One is taxed at exit. One is not. Twenty years later, the gap in your hand is not small. It can be lakhs.

The ULIP return calculator shows you this gap in black and white. Not theory. Actual numbers with your premium, your tenure, your tax bracket.

That is when people go, oh, I did not realise.

Insight 5: The Right Premium Amount for Your Goal

Here is a question worth asking yourself — do you invest and then see what you get? Or do you decide what you want and then figure out how to get there?

Most people do the first. It is easier.

But the second approach actually works better.

Pick a number. Say ₹50 lakh for your child's college in 15 years. Open the ULIP return calculator. Enter that as your target. Let it tell you what monthly or yearly premium gets you there.

No guessing. No hoping. Just a clear path from today to that number.

That is goal-based planning. And honestly, it is the only way a long-term product like a ULIP should be bought.

A Quick Comparison: What You Know vs What the Calculator Shows

Honestly, anyone who is considering a ULIP or already has one.

● New buyers: To understand what they are getting into

● Existing policyholders: To check if they are on track

● People comparing products: To see how ULIP stacks up against mutual funds or endowment plans

● Parents planning for children: To reverse-calculate the premium needed

Final Thought

Understanding the ULIP full form is just the starting point. It tells you what the product is called. It does not tell you whether it works for your life.

That is what the ULIP return calculator is for.

It turns a product name into a personal financial plan. It shows you the real numbers — charges, fund performance, tax savings, early exit impact, and goal tracking — all in one place.

Before you sign on the dotted line, spend ten minutes with the calculator.

Those ten minutes could save you from a twenty-year mistake. Or confirm that you are making a very smart decision.

ST Webdesk Verified Media or Organization • 13 Apr, 2026Editorial Desk

Sangri Today is a News Media website that covers the latest news in National, Politics, Rajasthan, Crime, Sports, Entertainment, Lifestyle, Business, Technology, and many more categories.

.jpeg)